What Is an SMSF?

Think of super like a piggy bank for retirement. Most Australians have their piggy bank run by a big super fund like AustralianSuper, Hostplus, or REST. With an SMSF (Self-Managed Super Fund), you run your own piggy bank. You decide what goes in, where it gets invested, and when to crack it open (in line with the rules). You’re in the driver’s seat but with that freedom comes responsibility.

Put simply: An SMSF is a private super fund that you manage yourself, regulated by the Australian Taxation Office (ATO).

Who Is an SMSF For?

An SMSF isn’t for everyone. They generally suit:

• Business owners who want to buy their own operating premises inside super.

• Property-focused investors who want to leverage super to buy real estate.

• High-balance individuals/couples (typically $200k+ combined, but realistically $500k+ makes the numbers work).

• Hands-on investors who want control over shares, property, or private assets.

Why Would You Have an SMSF?

SMSFs, give you control, flexibility, and tax benefits but only if managed correctly. Some of the key reasons Australians establish SMSFs include:

• Control –You pick the assets: property, shares, ETFs, cash, even crypto (within ATO rules).

• Flexibility – Borrow inside the SMSF under a Limited Recourse Borrowing Arrangement (LRBA).

• Property Access – Over 90% of SMSF borrowing is for direct property purchases.

• Business Benefits – Own your commercial premises inside super and rent it back at market rates.

• Tax Strategies – Pay 15% tax in accumulation and potentially 0% in pension phase.

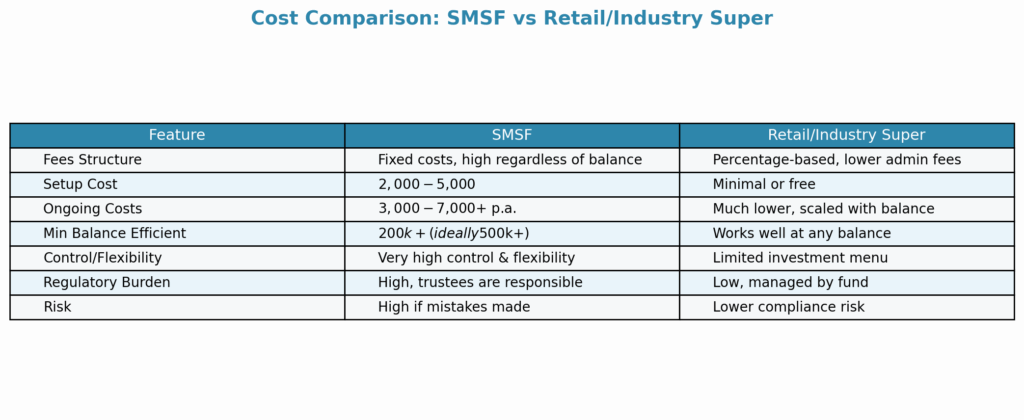

Costs: Setup & Ongoing

Setting up and running an SMSF comes with costs that can’t be ignored:

• Setup costs: $4,000–$8,000 (trust deed, company registration, ATO setup).

• Ongoing costs: $2,000–$7,000+ per year depending on complexity (audit, tax return, admin, investment costs).

For balances under ~$200k, these costs chew up returns. Over $500k, they often become efficient compared to retail fees.

Why a Corporate Trustee Beats Individual Trustees

Two structures are available: individual trustees or a corporate trustee. While the individual trustee route looks cheaper upfront, a corporate trustee is nearly always the superior option. It makes administration easier, avoids title change headaches (Trust me, this is painful if a member deceases), and is required if borrowing under an LRBA. It also provides greater asset protection.

Trust Deed: The Rulebook

Every SMSF must have a trust deed. This document governs how the fund operates: who can join, how decisions are made, and what investments are allowed. It’s essentially the constitution of your fund, and without it, nothing can proceed.

Borrowing Inside an SMSF: LRBAs Explained

An LRBA (Limited Recourse Borrowing Arrangement) allows an SMSF to borrow to purchase a single asset, most often property. The asset is held in a separate trust from the SMSF known as a BARE Trust or Holding Trust. The unique feature of an LRBA is that if the SMSF defaults, the lender can only access the asset securing the loan, they can’t touch other fund assets. This makes it safer for the fund as a whole while still allowing leverage inside super. However, lending rates inside the SMSF will always be higher as this is a significant risk to the lender. Additionally, lower LVR ratios are required by lenders to mitigate this risk. Currently (as of 22.09.25) no Big 4 lenders offer SMSF borrowing.

Example: SMSF buys a $700k commercial property. Members contribute $300k, the bank lends $400k. Rent and contributions pay down the loan. Once the loan is cleared, the property is owned outright within the SMSF. LVR under 60%

Using SMSFs for Property

Property is the number one reason many Australians open an SMSF. The appeal is clear:

• Tangible asset with rental income potential, long-term growth and the ability to leverage your retirement savings into an asset class with the hopes of growing your retirement savings.

• Ability to use leverage with an LRBA, that doesn’t affect your personal position.

• For business owners: Buying your premises through your SMSF allows you to own your workspace, not worry about relocating or the property being sold underneath you and allows you the freedom to grow the business without the fear that sunk costs into the property are gone forever. As the owner you rent it back to your business at market rates.

Investment Strategy: Non-Negotiable

Every SMSF must prepare and regularly review a written investment strategy. This strategy should outline:

• Member risk profiles and investment time horizons.

• Target asset allocation for the long-term benefit of its members.

• Liquidity requirements to pay member benefits and expenses of the fund.

• Insurance considerations for the members. This is a critically important step to consider, especially if borrowing inside the fund is undertaken.

The ATO and auditors will check compliance with your strategy each and every year. This step is the most important upon establishing the fund to ensure the SMSF remains compliant, but also as this is the long-term thinking behind how the fund should be invested.

Pros & Cons of SMSFs

Pros:

• Full control over investment choices.

• Ability to access property and borrowing strategies.

• Tax efficiencies inside super. Best tax rate in Australia with 15% in accumulation and 0% in retirement phase.

• Flexibility for estate planning.

Cons:

• Higher admin and compliance workload. An accountant can generally help with this compliance and admin workload at a cost.

• Expensive at lower balances. Not worth it for balances below $300,000 – $500,000

• Significant penalties for non-compliance: If the fund is non-compliant is does not qualify for concessional tax rates so its assessable income is taxed at the highest marginal tax rate, which is currently 45%

• Responsibility ultimately rests with the trustees.

Superannuation Industry Supervision (SIS) Rules to Know

The SIS Act 1993 is the legislative framework for SMSFs. It requires funds to:

• Ensure all investments are for retirement purposes, not personal benefit.

• Avoid lending to members or relatives.

· Meet the sole purpose test.

· Comply with investment restrictions.

· Prepare SMSF financials and lodge an annual tax return.

· Meet the residency rules.

• Follow rules around in-house assets and related-party transactions.

FAQs About SMSFs

Q: Can anyone start an SMSF?

A: Yes, but they usually make sense for higher balances (generally $200k+).

Q: How many members can an SMSF have?

A: Up to six members

Q: Are SMSFs risky?

A: The fund itself isn’t inherently risky. The risk comes from the investment choices made by the trustees.

Q: How much does it cost to set up an SMSF?

A: Between $4,000 and $8,000.

Q: Who set’s up an SMSF?

A: An accountant can set-up an SMSF. However, accountants can not give advice on superannuation or retirement savings and therefore they generally would refer to a financial advisor to ensure an SMSF is the right option for the members before they establish one.

Q: Do you need a financial advisor for an SMSF?

A: No. However, they are the only professional you can give superannuation advice. Consulting a financial advisor to ensure a SMSF is right for you is critical but not core to establishing an SMSF.

Final Thoughts

An SMSF can be a powerful wealth-building tool if managed well. It gives you control, flexibility, and strategic tax advantages, but it’s not a shortcut to easy money. For business owners and property investors, SMSFs can deliver outsized benefits. For others, an industry or retail super fund may be the smarter choice. SMSF’s aren’t for everybody! If you prefer simplicity then I would stay clear of an SMSF.

At Tenex Wealth, we help clients weigh up whether an SMSF is right for their circumstances or simply an expensive distraction.

Disclaimer

The information provided in this guide is general in nature and does not constitute personal financial advice. It is intended for educational purposes only and does not take into account your individual financial situation, objectives, or needs. Before making any financial decisions, consider seeking advice from a licensed financial adviser or tax professional. Tenex Wealth accepts no liability for reliance on this content.